The Gulf-Maghreb Strategic Realignment

Issue Brief, May 2026

Nonresident Senior Fellow

Key Takeaways

From Pan-Arab Solidarity to Project-Based Regionalism: Gulf–Maghreb relations no longer reflect formal integration drives, but a focus on distinct projects and sectoral cooperation. This offers flexibility, but limits institutional depth.

Divergences are Structural, Not Tactical: Disparities among Maghreb states in their Gulf engagement are not temporary or personality-driven. Rather, they reflect structural differences, threat perceptions, and economic strategies, as sovereignty management shapes external partnerships.

Gulf Capital Is Strategic but Not Transformative: Gulf investment has boosted struggling North African economies, yet remains selective and politically driven. While Gulf capital can support budgets, infrastructure, and regime resilience, it cannot substitute for structural reform or guarantee durable development.

Variable Geometry Dominates Ties: As multipolar competition intensifies and regional security frameworks erode, GCC–Maghreb ties will be flexible and focus on shared interests, rather than demanding regional cohesion. This will reduce over-commitment, but increases risks of fragmentation.

Introduction

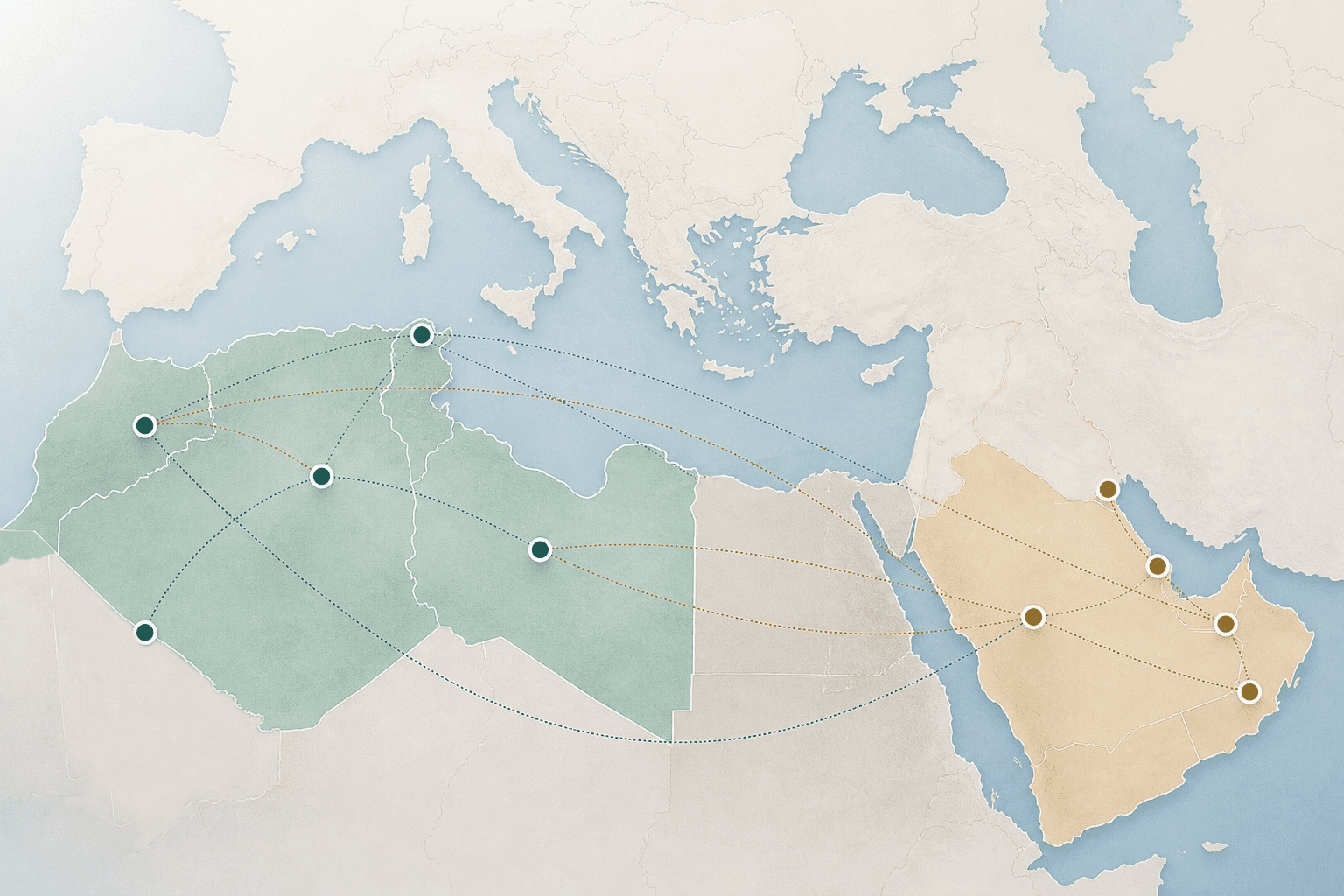

Over the past decade, Gulf-Maghreb relations have evolved from episodic diplomacy into dense networks of investment, migration, and security dialogue. This has produced a pragmatic form of inter-regional engagement driven by economic diversification, security externalities, and shifting global power balances. Gulf–Maghreb relations are increasingly structured around defined projects, sectors, and strategic economic corridors, such as port and logistics hubs, renewable energy, agribusiness, and digital infrastructure, rather than ideological alignments or formal integration.

This evolution reflects economic diversification on both sides. The Maghreb states, facing shifting dynamics with traditional Western partners and new global economic pressures, have diversified their international engagements by deepening ties with non-Western actors such as China and the Gulf states, as part of a broader strategy of transactional diplomacy and a quest for sovereign autonomy.1 Simultaneously, the Gulf states have intensified their engagement with the Maghreb as part of diversification strategies aimed at securing food supply chains, logistics hubs, energy partnerships, and access to African and Atlantic markets. The result is a complex but selective pattern of cooperation, in which economic instruments and security partnerships increasingly overlap.

This issue brief argues that contemporary Gulf–Maghreb relations are best understood as forms of flexible cooperation, without fixed alliances or institutionalized blocs. Rather than converging toward a unified regional order, the Gulf and Maghreb states are engaged in flexible, issue-specific alignments that allow cooperation where interests coincide and distance where they diverge. Economic pragmatism, regime security, and geopolitical hedging have replaced ideology as the primary drivers of inter-regional engagement.

From Episodic Diplomacy to Variable Geometry2

Over the past decade, relations between the Gulf and the Maghreb have shifted from episodic diplomacy toward denser, more institutionalized patterns of engagement. This reflects a reconfiguration of Arab inter-regionalism toward pragmatic, issue-driven cooperation, as opposed to a revival of pan-Arab bloc politics. Investment flows, labor mobility, security dialogue, and selective political coordination are taking precedence over formal treaties or ideological alignment.

Three structural forces underpin this evolution. First, the Gulf states—particularly Saudi Arabia, the United Arab Emirates, and Qatar—have pursued westward engagement as part of diversification strategies aimed at securing food supply chains, logistics corridors, energy partnerships, and access to African and Atlantic markets. Second, Maghreb governments, constrained by sluggish European demand and rising fiscal pressures, increasingly view Gulf capital as a stabilizing and comparatively non-conditional form of financing.3 Third, accelerating multipolarization—driven by energy shocks, technological disruption, and shifting great-power priorities—has encouraged flexible South–South partnerships rather than hierarchical dependency.4

Gulf policymakers increasingly view the Greater Maghreb5 as a connected strategic space linking the Mediterranean, the Sahel, and the Atlantic.6 Morocco and Mauritania function as Atlantic gateways; Algeria provides energy resources and military weight; Libya offers energy assets; Tunisia contributes human capital and technological potential. Yet this spatial logic does not translate into regional homogeny. Like their Gulf partners, each Maghreb state negotiates its own balance between sovereignty and interdependence, producing differentiated engagement with the Gulf—a dynamic reinforced by the enduring paralysis of the Arab Maghreb Union.

This relationship can be understood through the lens of “variable geometry,” a form of flexible cooperation where subsets of states deepen collaboration on shared interests but diverge in areas of political doctrine or threat perception—e.g. over sovereignty, ideology, security, and/or alignments. Instead of members of a bloc doing everything together at the same speed, smaller groups collaborate on certain projects or policies, based on their respective interests and capacities.

The result is a networked form of regionalism organized around shared interests. Memoranda of understanding, sovereign-fund ventures, joint training programs, and targeted investments have become the dominant instruments of engagement.

In the Gulf, economic diversification, population growth, and decarbonization generate outward investment pressures and a search for strategic depth beyond the Arabian Peninsula.7 Taken together, this produces cooperation that is transactional but durable, selective yet strategic. Rather than disengagement from core security theaters, the Gulf’s growing presence in the Maghreb illustrates a broader strategy of risk distribution: combining high-stakes geopolitical involvement with lower-volatility economic expansion in North Africa.

The following case studies illustrate how this variable-geometry regionalism operates in practice, as individual Maghreb states engage the Gulf through distinct combinations of economic pragmatism, security cooperation, and sovereignty management.

Morocco: Strategic Alignment with Managed Autonomy

Among the Maghreb states, Morocco maintains the deepest and most institutionalized relations with the Gulf monarchies.8 Since the 1970s, Rabat has cultivated a narrative of Arab monarchical fraternity rooted in dynastic legitimacy, religious kinship, and regime continuity. This symbolic proximity has translated into sustained political support and significant economic engagement, particularly with Saudi Arabia, the UAE, and Qatar.

Gulf backing for Morocco’s territorial claims over the Western Sahara has been a central pillar of this relationship.9 Over the past decade, and especially since 2020, Gulf states have consistently endorsed Rabat’s plan for the territory—autonomy under Moroccan sovereignty—at international fora.10 This political solidarity has been complemented by Gulf investments in infrastructure, tourism, logistics, and energy, positioning Morocco as a preferred gateway for Gulf capital into Atlantic Africa.11

At the economic level,12 Morocco has framed Gulf engagement as a component of its broader strategy of diversification—into ports and logistics, renewables, agribusiness, and manufacturing—and external balancing, by seeking partners beyond Europe.13 Emirati and Saudi investments have targeted ports, industrial zones, utilities, renewable energy, and agribusiness, aligning with Morocco’s ambition to consolidate its role as a logistics hub.14 Unlike in other Maghreb states, Gulf capital in Morocco has been broadly welcomed and institutionalized, reflecting high levels of political trust and policy alignment.15

These relationships also involve security cooperation. Rabat has cultivated close ties with Gulf defense establishments through joint exercises, intelligence exchanges, and participation in Gulf-led security initiatives.16 Normalization with Israel17 under U.S. auspices has added a new dimension to this alignment, enabling trilateral cooperation in defense technology, cybersecurity, and intelligence.18 During the 2017 Gulf crisis, Rabat remained neutral, maintaining relations with Qatar and offering to mediate,19 reflecting a broader strategy of bridge-building and diplomatic hedging.

Overall, Morocco’s Gulf engagement illustrates variable geometry at its most cooperative. Shared political interests, geopolitical alignment, and economic complementarity have produced a dense partnership, even as Rabat preserves room for maneuver and avoids full strategic dependence. Morocco thus represents the most advanced form of GCC–Maghreb alignment—one shaped by careful sovereignty management rather than unconditional alignment.

Algeria: Realism and Selective Convergence

Algeria’s engagement with the Gulf is best understood through the dual lenses of sovereigntist realism and variable geometry. Since late 2019, Algeria has become increasingly economically assertive while maintaining strict limits on its sovereignty, territorial integrity, and external interference. Its material engagement with Gulf partners has expanded, but without ideological alignment or bloc integration.

Energy is the most structured and durable pillar of Algeria–Gulf relations. Within OPEC+, Algeria coordinates closely with Saudi Arabia and the UAE on output management and price stabilization. In November 2024, all three were among eight producers that extended voluntary output cuts to the year’s end;20 in March 2025, the same group collectively agreed to increase daily production.21 This institutionalized coordination underscores a central dynamic. Algeria and major Gulf producers remain embedded in shared energy governance mechanisms and OPEC+ provides a stabilizing, multilateral framework that cushions broader geopolitical differences.

Algeria’s ties with Saudi Arabia reflect calibrated economic pragmatism rather than strategic realignment. State oil giant Sonatrach’s $5.4-billion, 30-year production-sharing agreement with Saudi firm Midad Energy North Africa over the Illizi Basin in October 2025 is a case in point; it includes full Saudi financing, a seven-year exploration phase, and projected resources approaching 993 million barrels of oil equivalent.22 This agreement gives Algeria access to Gulf capital while preserving state control through production-sharing architecture.

Qatar is more structurally compatible with Algeria, with the relationship anchored in long-term industrial cooperation. Algerian Qatari Steel (AQS), established through agreements between Qatar International, a joint venture between Qatar Steel and Qatar Mining, and Algerian partners,23 is the flagship of their bilateral ties. In 2023, the company reported transactions of around $1.2 billion, with plans to double capacity from two million tons of final iron products annually to four million tons.24

This engagement has since expanded into strategic agriculture. In April 2024, Qatari dairy firm Baladna signed an agreement with Algeria’s Ministry of Agriculture for a $3.5 billion integrated dairy project aimed at reducing milk powder imports.25 These investments align with Algeria’s food security strategy and import-substitution agenda. While the Gulf attracts relatively fewer Algerian labor compared to Europe.26 Though small, this social layer complements industrial and diplomatic engagement.

Algeria’s selective convergence with Qatar, Kuwait,27 Saudi Arabia, and Oman28 contrasts starkly with its complicated relationship with the UAE, which by early 2026 Algiers was reportedly considering severing entirely.29 Since 2024, Algeria has increasingly interpreted Emirati regional activism, particularly in Libya and the Sahel, as incompatible with its own sovereignty.

This mistrust is amplified by developments in the Sahel and Libya—both integral to Algeria’s security perimeter. Since 2023, the erosion of multilateral Sahel security frameworks and strained relations with military-led authorities in Mali and Niger30 have heightened Algerian sensitivity to external involvement. The tension reflects deeper structural differences: Algeria emphasizes negotiated settlements and non-intervention, while the UAE’s regional alignments—such as Abu Dhabi’s alignment with Algeria’s arch-rival Morocco—has generated friction. In the variable geometry framework, cooperation slows where threat perceptions diverge. The rift is less episodic than structural, rooted in competing security doctrines and influence strategies, and sharpened by Abu Dhabi’s close partnership with Morocco and role in Libya.

Tunisia: Aid without Alignment

Since 2020, Tunisia has sought Gulf support to stabilize its fragile economy, while carefully avoiding political or security alignment.31 Successive Tunisian governments have framed relations with Gulf partners as strictly transactional, emphasizing financial assistance, investment, and humanitarian support rather than strategic partnership.

Qatar remains Tunisia’s most trusted Gulf interlocutor.32 While Doha’s billion-dollar pledges of the mid-2010s (including a reported $1.25 billion aid package in 2016) did not fully materialize, the Qatari approach has generally been low-conditionality and non-ideological.33 This has enabled Tunis to secure external resources without overtly compromising its diplomatic autonomy or becoming entangled in intra-Gulf rivalries.

Tunisia’s financial needs, however, have been acute. In July 2023, Saudi Arabia provided a $400-million soft loan and $100-million grant to help shore up Tunisia’s public finances, hit by debt pressures and stalled International Monetary Fund (IMF) negotiations.34 Saudi development bodies have also cooperated with Tunisian planning authorities on smaller assistance, such as a $38-million concessional loan in June 2025 to support rural infrastructure, housing, and social facilities in underserved southern regions,35 reflecting a long-standing Saudi development footprint in Tunisia.

The UAE and Kuwait have also engaged Tunisia through financial and project-level support, though on a more limited and cautious basis. Gulf sovereign wealth funds have discussed or committed financing for infrastructure projects including transport upgrades, water desalination, and support for businesses, but execution has been uneven. Emirati financing institutions include Tunisian engagements among their broader Arab development initiatives.36

Despite these inflows, Tunisian policymakers have resisted deeper political alignment. This reflects acute concerns over domestic legitimacy and widespread public skepticism toward external political influence, especially after contested constitutional changes and stalled IMF talks. Tunisia’s leadership has repeatedly stressed that conditional agreements with the IMF, particularly those involving subsidy cuts or structural reforms, risk social unrest. This underscores the fragile political economy within which Gulf support is negotiated.37 As a result, Gulf assistance in Tunisia is treated as a fiscal buffer, not a vehicle for strategic realignment.

Tunisia’s diplomatic posture has emphasized neutrality and balance. Even amid fiscal stress, Tunis has avoided endorsing Gulf-led regional initiatives that could be perceived as politically binding, including formal security frameworks, politically charged economic platforms, or explicit alignment in intra-Arab disputes.

Economically, Tunisian authorities have favored ad-hoc financial support over institutionalized strategic partnerships, avoiding comprehensive agreements that would tie economic assistance to political alignment.

All this reflects Tunisian concerns about being drawn into geopolitical contestation. That said, it has developed limited, technical security cooperation with some Gulf states, particularly in areas such as training and counterterrorism exchanges with partners including Bahrain.38 However, these remain low-profile and narrowly defined.

The absence of large-scale transformative Gulf investment, in contrast to Egypt, for example, highlights the limits of Tunisia’s leverage. Gulf capital and development financing can ameliorate short-term fiscal disruption, but they have not catalyzed structural economic transformation or long-term development momentum. Tunisia therefore represents a minimalist version of variable geometry; its Gulf cooperation is narrowly focused on economic survival and specific development projects.

Libya: Competition and Managed Recalibration

Libya remains the clearest illustration of how Gulf–Maghreb relations can evolve into competitive, rather than cooperative, engagement. For the Gulf states, Libya is both a security theater and a test for competing models of regional order.39 For the Maghreb states—especially Algeria—it represents a source of persistent instability, with direct security spillovers.

The UAE has been the most active Gulf actor in Libya.40 During the 2019–2020 conflict, Abu Dhabi emerged as a key supporter of eastern Libyan forces aligned with Khalifa Haftar. This clashed with UN-backed mediation efforts and deepened Libya’s fragmentation, reinforcing Algerian concerns about militarized external intervention along its eastern border. Qatar, by contrast, has maintained ties with Tripoli-based authorities and positioned itself as a supporter of political dialogue and institutional continuity. While Doha’s recent role has been more restrained than in earlier phases of the conflict, its engagement underscores the persistence of parallel Gulf patronage networks in Libya’s fractured political landscape.

Saudi Arabia’s role has been more limited, focusing on diplomatic engagement and support for UN-led processes, which reflects a broader recalibration toward de-escalation and mediation following years of regional overstretch.41 Since 2021, reconciliation with Qatar has reduced overt confrontation among the Gulf states in Libya, but it has not eliminated their competitive influence. Emirati diplomacy has adopted a more cautious public tone, emphasizing dialogue and stability, yet the legacy of earlier intervention continues to shape Libyan dynamics and regional perceptions. Gulf engagement in Libya remains characterized by hedging rather than withdrawal.

Libya thus occupies an intermediate position in GCC–Maghreb relations. It is neither a site of deep alignment nor one of outright disengagement, but rather a hybrid arena where Gulf states are recalibrating their strategies, within constraints. The Libyan case highlights the limits of Gulf power projection and the enduring costs of competitive external involvement in fragile political systems.

Mauritania: Strategic Visibility at the Sahel’s Margin

Long peripheral to Gulf–Maghreb relations, Mauritania has gained strategic visibility over the past decade as a relatively stable actor at the intersection of the Maghreb, the Sahel, and the Atlantic. Its political continuity and growing role in regional security have made it an increasingly attractive partner for Gulf states seeking influence in West Africa without the risks associated with more volatile theatres.

Qatar has been central to Mauritania’s renewed Gulf engagement. Despite Nouakchott aligning with Doha’s rivals in 2017 by cutting diplomatic ties and halting transport links, relations were restored in 2021 with the reopening of Qatar’s embassy.42 Qatar has since pledged substantial support for infrastructure, social development, and humanitarian projects.43

Saudi Arabia and the UAE have focused primarily on security cooperation, supporting counterterrorism capacity-building, border security initiatives, and institutional support linked to Sahel stabilization efforts.44 While Mauritania’s participation in multilateral Sahelian frameworks has evolved as regional mechanisms deteriorate, Nouakchott continues to position itself as a reliable interlocutor capable of navigating between regional actors and external partners.45 Mauritania contributes practical expertise in desert warfare, intelligence-sharing, and security coordination, while Gulf partners provide financing, equipment, and political backing. This reflects a pragmatic security partnership rather than ideological alignment, consistent with Mauritania’s broader diplomatic posture.

Strategically, Mauritania’s importance lies less in its economic weight than its functional utility. As Sahelian multilateralism fragments and state-centric security arrangements replace collective frameworks, Mauritania offers Gulf states a stable platform for engagement at the western edge of the region.46 For Nouakchott, Gulf cooperation enhances regime stability and international visibility without binding the country to rigid alliances. Since 2023, Saudi, Qatari, and Emirati funds have supported counterterrorism training centers, border-security technologies, and coastal surveillance programs in Mauritania.47 This pragmatic arrangement sees Gulf partners supplying capital and equipment, while Mauritania offers field expertise, intelligence-sharing, and regional access.48

Mauritania thus exemplifies a minimalist but effective form of variable geometry. Engagement with the Gulf is selective, security-focused, and calibrated to preserve sovereignty, underscoring how smaller Maghreb states can leverage their strategic location and experience to gain relevance in a shifting regional order.

The Maghreb and the U.S.-Israel-Iran War: Selective Condemnation and Strategic Silence

Maghreb responses to the February 2026 escalation revealed a notable asymmetry: while most states expressed solidarity with the Gulf states following Iran’s strikes, they remained largely silent on the initial U.S.–Israeli attacks on Iran.49

Morocco and Algeria avoided condemning the U.S.–Israeli strikes50 reflecting broader strategic calculations linked to relations with Washington and regional priorities such as the Western Sahara. This selective positioning was also observed by Tunisia51 and Mauritania,52 which condemned aggression against Arab states while refraining from directly addressing the U.S.-Israeli attacks on Iran. Conversely, Libya’s internationally recognized authorities in Tripoli condemned both the U.S.–Israeli strikes and Iran’s retaliation, calling for dialogue and de-escalation.53

Conclusion

GCC–Maghreb relations have entered a phase defined not by ideological alignment or bloc formation, but by calibrated, interest-driven engagement. Across the Maghreb, Gulf partnerships are structured around national priorities, rather than embedded in a unified regional posture.

This differentiation highlights structural realities. Cooperation advances where material interests align—energy governance, infrastructure, logistics, fiscal stabilization—and slows where sovereignty doctrines, threat perceptions, or regional ambitions diverge. The result is a web of adaptive partnerships, rather than a cohesive inter-regional architecture.

Absent a shared institutional framework or unified strategic vision, GCC–Maghreb relations are unlikely to crystallize into a coherent regional order. Instead, they will remain flexible, transactional, and strategically hedged, shaped by domestic constraints, shifting security landscapes, and the broader multipolar reconfiguration of global politics.

For policymakers, the implication is clear: the future of Gulf–Maghreb engagement lies not in constructing formal blocs, but in managing asymmetries, mitigating friction, and institutionalizing pragmatic cooperation where interests converge. Stability will depend less on grand regional design and more on disciplined, sector-specific coordination within an increasingly competitive geopolitical environment.

References

1 Intissar Fakir, Sovereignty first: Reshaping international cooperation in North Africa (Washington, D.C., Middle East Institute, March 24, 2025), https://mei.edu/publication/sovereignty-first-reshaping-international-cooperation-north-africa/.

2 Peter Lloyd, “The Variable Geometry Approach to International Economic Integration,” International Journal of Business and Development Studies, 2010, https://ijbds.usb.ac.ir/article_1304_cf58b15ac0cec6fb55a894e891cb0520.pdf.

3 Karim Mezran and Sabina Henneberg, Gulf Influence in the Maghreb (Washington, D.C., New Lines Institute, June 1, 2022), https://newlinesinstitute.org/state-resilience-fragility/gulf-influence-in-the-maghreb/.

4 Elham Fakhro and Peter Salisbury, “The Gulf States in the Multipolar Transition,” POMEPS, February 11, 2025, https://pomeps.org/the-gulf-states-in-the-multipolar-transition.

5 The Greater Maghreb refers to Algeria, Libya, Mauritania, Morocco, and Tunisia. Before 1989 and the creation of the Arab Maghreb Union (UMA), the Maghreb usually referred to Algeria, Morocco, and Tunisia.

6 International Monetary Fund, Regional Economic Outlook: Middle East and Central Asia (2024–2025 editions), https://www.imf.org/en/publications/reo/meca.

7 Aisha Al-Sarihi, Gulf Transition to Low-Carbon Economies: The Role of Carbon Markets, Issue Brief (Doha: Middle East Council on Global Affairs, November 2024), https://mecouncil.org/publication/gulf-transition-to-low-carbon-economies-the-role-of-carbon-markets/.

8 Morocco’s Middle East Positioning: Balancing Gulf Partnerships and Regional Tensions, Policy Brief 04 (n.p., Konrad Adenauer Stiftung, July 29, 2025), https://www.kas.de/documents/276068/36100580/Morocco_Radar_N4_V0.90.pdf/21e48491-5c37-83a8-8734-bc8bef97c91a?version=1.0&t=1753802075984.

9 “GCC backs Morocco’s sovereignty over Western Sahara Amid UN endorsement,” Africa News, December 5, 2025, https://www.africanews.com/2025/12/04/gcc-backs-moroccos-sovereignty-over-western-sahara-amid-un-endorsement/.

10 Giorgio Cafiero, “Gulf States Embolden Morocco as Temperatures Rise in Western Sahara,” Gulf International Forum, December 31, 2020, https://gulfif.org/gulf-states-embolden-morocco-as-temperatures-rise-in-western-sahara/.

11 Morocco’s Middle East Positioning.

12 In 2024, Morocco had significant bilateral trade with key Gulf partners: Exports to the UAE stood at roughly $275 million and exports to Saudi were around $185 million. Imports from Saudi Arabia were around $2.87 billion and the UAE $1.73 billion. Together, these figures reflect the magnitude of Morocco’s trade relations with major Gulf economies.

13 Trading Economics, “Morocco,” accessed March 10, 2026, https://tradingeconomics.com/morocco/.

14 Dakir Madiha, “Morocco and the Gulf: forging a strategic economic alliance,” Walaw, September 2, 2025, https://en.walaw.press/country/hicham_telmoudi/QWSP/articles/morocco_and_the_gulf_forging_a_strategic_economic_alliance/GQGWMMWXLPWL; Anchal Kapadia, “Historic $14 Bn Deal Between Morocco and UAE Announced,” MEP Middle East, May 29, 2025, https://www.mepmiddleeast.com/news/historic-deal-between-morocco-and-uae.

15 Jaber Mohamed Al Shuaibi, “Morocco and the Arab Gulf: Building a Strategic Economic Bridge,” Morocco World News, September 1, 2025, https://www.moroccoworldnews.com/2025/09/256422/morocco-and-the-arab-gulf-building-a-strategic-economic-bridge/.

16 Raúl Redondo, “Morocco and Saudi Arabia reinforce security partnership,” Atalayar, February 5, 2024, https://www.atalayar.com/en/articulo/politics/morocco-and-saudi-arabia-reinforce-security-partnership/20240205124430196510.html.

17 The Abraham Accords (2020) transformed normalization with Israel into a broader geopolitical framework combining economic, security, and diplomatic cooperation. Morocco aligned with the UAE–Bahrain track, normalizing relations with Israel, despite persistent opposition to normalization by its own public and governments across much of North Africa.

18 “After meeting in Rabat, Morocco agrees to boost military ties with Israel,” The Arab Weekly, January 18, 2023, https://thearabweekly.com/after-meeting-rabat-morocco-agrees-boost-military-ties-israel.

19 “Morocco offers to mediate Qatar-GCC crisis,” Al Jazeera, June 11, 2017, https://www.aljazeera.com/news/2017/6/11/morocco-offers-to-mediate-qatar-gcc-crisis; Anna Jacobs, “Strategic Interests Spark Shift in Morocco’s Gulf Ties,” Arab Gulf States Institute, November 4, 2020, https://agsi.org/analysis/strategic-interests-spark-shift-in-moroccos-gulf-ties/.

20 OPEC, “Saudi Arabia, Russia, Iraq, the United Arab Emirates, Kuwait, Kazakhstan, Algeria, and Oman extend the 2.2 mbd voluntary adjustments,” Press Release, November 3, 2024, https://www.opec.org/pr-detail/23-03-nov-2024.html.

21 OPEC, “Saudi Arabia, Russia, Iraq, the United Arab Emirates, Kuwait, Kazakhstan, Algeria, and Oman reaffirm commitment to market stability on healthier oil market outlook,” Press Release, March 3, 2025, https://www.opec.org/pr-detail/518-03-march-2025.html.

22 “Algeria signs $5.4 billion oil & gas deal with Saudi firm Midad Energy,” Reuters, October 13, 2025, https://www.reuters.com/business/energy/algeria-signs-54-billion-oil-gas-deal-with-saudi-firm-midad-energy-2025-10-13/; Sonatrach, “Sonatrach – Midad Energy North Africa Sign hydrocarbon contract in the perimeter of Illizi South,” press release, October 13, 2025, https://sonatrach.com/en/sonatrach-midad-energy-north-africa-sign-hydrocarbon-contract-in-the-perimeter-of-illizi-south/.

23 “Qatar Steel, Qatar Mining get Algeria steel plant deal,” Reuters, November 8, 2012, https://www.reuters.com/article/steel-qatar-algeria/update-1-qatar-steel-qatar-mining-get-algeria-steel-plant-deal-idUSL5E8M8CIL20121108/.

24 “AQS General Manager to QNA: Company’s Transactions Reached Around $1.2 Billion in 2023,” Qatar News Agency, February 28, 2024, https://qna.org.qa/en/news/news-details?id=0024-aqs-general-manager-to-qna-company%27s-transactions-reached-around-$12-billion-in-2023&date=28/02/2024.

25 Baladna, “Baladna Q.P.S.C. Signs an Agreement with Algeria’s Ministry of Agriculture,” Press Release, April 25, 2024, https://baladna.com/en/baladna-qpsc-signs-an-agreement-with-the-algerian-ministry-of-agriculture; GEA, “GEA mandated to build world’s largest integrated dairy facility in Algeria,” press release, July 29, 2025, https://www.gea.com/en/news/corporate/2025/algeria-worlds-largest-dairy-facility/.

26 Gulf Labour Markets and Migration (GLMM) Programme, “Qatar: Estimates of foreign residents by country of citizenship,” https://gulfmigration.grc.net/qatar-estimates-foreign-residents-qatar-country-citizenship-selected-countries-c-2015-2016/.

27 “Relations with Kuwait ‘strong and distinct’: Algerian ambassador,” Arab Times, November 4, 2025, https://www.arabtimesonline.com/news/relations-with-kuwait-strong-and-distinct-algerian-ambassador/.

28 “Oman, Algeria Committed to Maintaining Strong Relations,” Oman Daily Observer, October 28, 2024, https://www.omanobserver.om/article/1161292/opinion/oman/oman-algeria-committed-to-maintaining-strong-relations.

29 “Algeria could sever ties with UAE ‘in the coming days’ amid links to separatists,” Middle East Eye, January 7, 2026, https://www.middleeasteye.net/news/algeria-could-sever-ties-uae-coming-days-media-report.

30 Yahia H. Zoubir, Crisis in the Sahel: Causes, Consequences, and the Path Forward, Issue Brief (Doha: Middle East Council on Global Affairs, June 2022), https://mecouncil.org/wp-content/uploads/2022/06/MECGA_Issue-Brief_Zoubir_Final.pdf.

31 Anna L. Jacobs, “Qatar-Tunisia Ties Spur Competition with Gulf Arab Neighbors,” Arab Gulf States Institute, December 14, 2020, https://agsi.org/analysis/qatar-tunisia-ties-spur-competition-with-gulf-arab-neighbors/.

32 Sebastian Sons, “Gulf engagement in Tunisia: Past endeavor or future prospect?,” Atlantic Council, August 3, 2023, https://www.atlanticcouncil.org/in-depth-research-reports/report/tunisia-gulf-engagment-future/.

33 “Qatar to give $1.25 billion of aid to Tunisia: Emir,” Reuters, November 29, 2016, https://www.reuters.com/article/world/qatar-to-give-1-25-billion-of-aid-to-tunisia-emir-idUSL8N1DU2DG/.

34 “Saudi Arabia to give Tunisia $500 million as soft loan and grant,” Reuters, July 20, 2023, https://www.reuters.com/world/saudi-arabia-give-tunisia-500-mln-soft-loan-grant-2023-07-20/.

35 “Saudi fund signs $38 million loan to boost rural infrastructure in Tunisia,” The Arab Weekly, June 30, 2025, https://thearabweekly.com/saudi-fund-signs-38-million-loan-boost-rural-infrastructure-tunisia.

36 “Coopération économique entre la Tunisie et les marchés du Golfe : Une dynamique en marche [Economic cooperation between Tunisia and the Gulf markets: A dynamic in progress],” La Presse (Tunisie), March 17, 2025, https://www.lapresse.tn/2025/03/17/cooperation-economique-entre-la-tunisie-et-les-marches-du-golfe-une-dynamique-en-marche/.

37 Faïrouz ben Salah, “Coups, fake footage and proxy parties: What is the UAE doing in Tunisia?,” Libya Tribune, July 27, 2021, https://en.minbarlibya.org/2021/07/27/coups-fake-footage-and-proxy-parties-what-is-the-uae-doing-in-tunisia/.

38 “Bahrain, Tunisia Review Security Cooperation and Citizen Services,” Gulf Press, January 17, 2026, https://gulfpress.net/bahrain-tunisia-review-security-cooperation-and-citizen-services/.

39 Anna L. Jacobs, “Gulf Rivalries and Great Power Competition in Libya,” Arab Gulf States Institute, June 8, 2020, https://agsi.org/analysis/gulf-rivalries-and-great-power-competition-in-libya/.

40 Abdulkader Assad, “The UAE’s Libya Bet Is Becoming a Regional Liability,” Libya Observer, January 24, 2026, https://libyaobserver.ly/opinions/uaes-libya-bet-becoming-regional-liability.

41 “Saudi Arabia, UN Discuss Ways to Revive Libya’s Political Roadmap,” Asharq Al-Awsat, October 22, 2025, https://english.aawsat.com/gulf/5200047-saudi-arabia-un-discuss-ways-revive-libya%E2%80%99s-political-roadmap.

42 “Mauritania re-establishes diplomatic ties with Qatar,” Al Jazeera, March 22, 2021, https://www.aljazeera.com/news/2021/3/22/mauritania-re-establishes-diplomatic-ties-with-qatar.

43 International Federation of Red Cross and Red Crescent Societies (IFRC), Mauritania: 2025-2026 IFRC Network Country Plan (n.p., IFRC, June 13, 2025), https://go-api.ifrc.org/api/downloadfile/91383/Mauritania_INP_2025.

44 Albert Vidal, “The GCC and sub-Saharan Security: Equipment Supplies Above All,” ISPI, September 30, 2024, https://www.ispionline.it/en/publication/the-gcc-and-sub-saharan-security-equipment-supplies-above-all-184869.

45 U.S. Department of State, Country Reports on Terrorism 2023: Mauritania (Washington, D.C., U.S. Department of State, 2024), https://2021-2025.state.gov/reports/country-reports-on-terrorism-2023/mauritania/.

46 Jean-Loup Samaan, “Gulf Countries and the Stabilization Efforts in the Sahel,” AGDA Insight (Abu Dhabi: Anwar Gargash Diplomatic Academy, November 2021), https://www.agda.ac.ae/docs/default-source/Publications/dr-jean-loup-samaan-english-01.pdf.

47 Niagalé Bagayoko, Presence and influence of the Middle Eastern powers in sub-Saharan Africa (Toulon, France: Mediterranean Foundation for Strategic Studies, February 5, 2025), https://fmes-france.org/en/presence-and-influence-of-the-middle-eastern-powers-in-sub-saharan-africa/.

48 Samaan, “Gulf Countries.”

49 Khadidja Mohsen-Finan, “Guerre en Iran. Le Maghreb se refuse à condamner les États-Unis [War in Iran. The Maghreb refuses to condemn the United States],” Orient XXI, March 24, 2026, https://orientxxi.info/Guerre-en-Iran-Le-Maghreb-se-refuse-a-condamner-les-Etats-Unis.

50 Rafik Tadjer, “L’Algérie juge ‘inacceptables’ les agressions iraniennes contre les pays arabes [Algeria considers Iranian aggression against Arab countries ‘unacceptable’],” TSA, March 29, 2026, https://www.tsa-algerie.com/lalgerie-juge-inacceptables-les-agressions-iraniennes-contre-les-pays-arabes/.

51 “Tunisia rejects aggression against Arab states amid regional escalation,” SANA, March 1, 2026, https://sana.sy/en/international/2299512/.

52 “Mauritania Strongly Condemns Iranian Aggressions Against Brotherly Arab States,” Agence Mauritanienne d’Information, March 1, 2026, https://ami.mr/en/archives/30429.

53 Safa Alharathy, “Libya condemns Israeli strike on Iran and retaliatory attacks, urges dialogue,” The Libya Observer, March 1, 2026, https://libyaobserver.ly/inbrief/libya-condemns-israeli-strike-iran-urges-dialogue.

Related

Publications

view more

China’s engagement with the Maghreb represents a strategic expansion of its Africa and Mediterranean policy, emphasizing infrastructure, resource security, and balanced diplomacy.

learn more

In recent years, Algeria and neighboring Mali have clashed repeatedly, in a string of diplomatic disagreements and security incidents with major implications for stability in the broader Sahel region. The…

learn more

This is the second dossier of a multi-year project entitled, "The Future of the Mediterranean (dis)Order.” The first dossier analyzed the ongoing regional reset and emerging multipolarity, assessing their impact…

learn more